Credit card debt can cast a shadow over one’s financial well-being. Credit cards usually have steep interest rates and penalties for late payments. Due to late fees and interest, credit card debt can increase even if you are not making new charges leading you down a path of financial ruin.

Understanding the Causes of Credit Card Debt

Credit card debt is often the result of unforeseen circumstances and financial mismanagement:

- Unplanned Expenses: Unexpected medical bills, car repairs, or other emergencies can quickly lead to the use of credit cards to cover immediate costs.

- Lack of Budgeting: Failing to create and adhere to a budget can result in overspending and reliance on credit cards to bridge the gap between income and expenses.

- High-Interest Rates: Credit cards typically come with high-interest rates, making it challenging to pay off the balance, especially if only minimum payments are made.

- Job Loss or Income Reduction: A sudden loss of employment or a reduction in income can make it difficult to meet financial obligations, leading to increased reliance on credit cards.

The Impact

Carrying a significant amount of credit card debt can have severe consequences:

- Financial Stress: Constant worry about debt can lead to stress, anxiety, and even negatively impact physical health.

- Credit Score Impact: High credit card balances can lower credit scores, making it challenging to secure favorable interest rates on loans or obtain new credit.

- Interest Accumulation: High-interest rates mean that a substantial portion of payments goes towards interest rather than reducing the principal amount owed, causing the debt to linger.

Strategies for Managing Credit Card Debt

- Create a Budget: Develop a realistic budget that includes all income and expenses. This helps identify areas where spending can be reduced and allows for a structured debt repayment plan.

- Emergency Fund: Establishing an emergency fund can provide a financial safety net, reducing the need to rely on credit cards for unexpected expenses.

- Negotiate Interest Rates: Contact credit card companies to negotiate lower interest rates. A lower rate can significantly reduce the overall cost of paying down the debt.

- Debt Snowball or Avalanche Method: Choose a debt repayment strategy that works best for your situation. The debt snowball method involves paying off the smallest debts first, while the debt avalanche method focuses on paying off high-interest debts first.

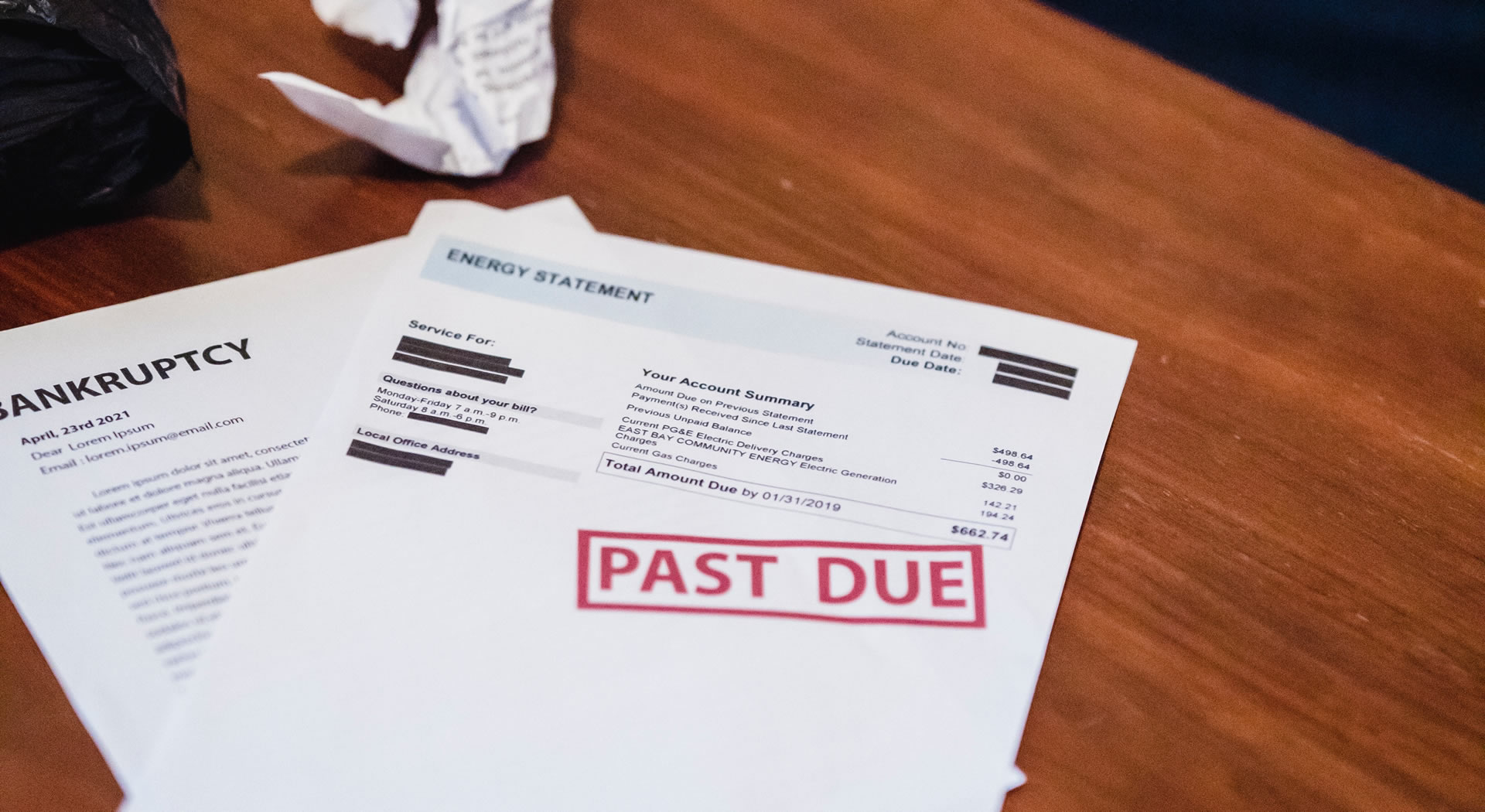

Eliminating All Credit Card Debt

Credit card debt is considered unsecured debt, meaning it is not backed by collateral. In the context of bankruptcy, unsecured debts can be eliminated, providing a clean slate to the debtor. There are two primary types of bankruptcy for individuals:

- Chapter 7 Bankruptcy: Also known as liquidation bankruptcy, Chapter 7 involves the sale of non-exempt assets to pay off creditors. Credit card debt is typically discharged in this process, offering individuals a clean slate.

- Chapter 13 Bankruptcy: This form of bankruptcy involves creating a repayment plan, allowing the debtor to repay a portion or all of their debts over a specified period, usually three to five years. Credit card debt may be reduced, and remaining balances are often discharged at the end of the plan.

While credit card debt is a serious financial challenge, I encourage you to reach out to me for professional advice for your individual situation. Together, we can explore alternative solutions in addition to bankruptcy & see which will best benefit you. I will work with you to create a plan where the goal is to get rid of your debt and get you back on track financially.

I’ll help you take the first step towards regaining your financial freedom. To schedule a consultation, fill out the online form or call me at (410) 486-3500.